UPS (UPS) rose 10% on a massive drop in expenses and raised 2025 guidance amid ongoing cost reduction, making good on its promises.

United Parcel Services UPS $96 Up 10% after a solid earnings beat.

September Quarter Results

Q3 Non-GAAP EPS of $1.74 beats handily by $0.44.

Revenue of $21.4B (-3.6% Y/Y) beats by $560M. - Note, this is a revenue decrease but still better than expectations. Revenue growth remains a problem because of US / China trade and the reduction in Amazon deliveries.

Guidance and estimates: Q4-2025

Revenue estimated at $24.0Bn, non-GAAP adjusted operating margin 11.0% - 11.5%, and Adjusted EPS of $2.41 - 20% drop YoY.

Guidance and estimates: Full year 2025:

UPS took a hatchet to jobs, and eliminated 34,000 this year, 70% higher than planned, most of which were drivers and package handlers. Further, in an effort to save costs, it closed daily operations at 93 leased and owned buildings in 2025. Since its planning to and has reduced its Amazon dependency in favor of higher margin medical deliveries, this was a necessary step.

The total cost-reduction has saved an estimated $2.2Bn in the first 9 months, with an additional $1.3Bn expected in Q4-2025 to a total of $3.2Bn for the year.

Siebert Financial likes it but meeds more:

The quarterly results were “impressive,” but one good report “may not be enough to turn the massive ship around,” said Mark Malek, chief investment officer at Siebert Financial. “The company has been clearly struggling with growth, even prior to this tariff regime. Pressure from competition and emergence of AI to optimize supply chains is mounting.”

Valuation: Cost reduction helps, specially when its in Billions, but UPS needs to show growth to attract buyers. The valuation is not bad at 13x earnings estimated to grow at about 8% in the next 3-4 years and 1x sales estimated to grow at 2%.

We had a previous report on UPS on 9/15, as a cautious Buy, indicating that UPS had a limited downside at $85, and that the dividend looked safe.

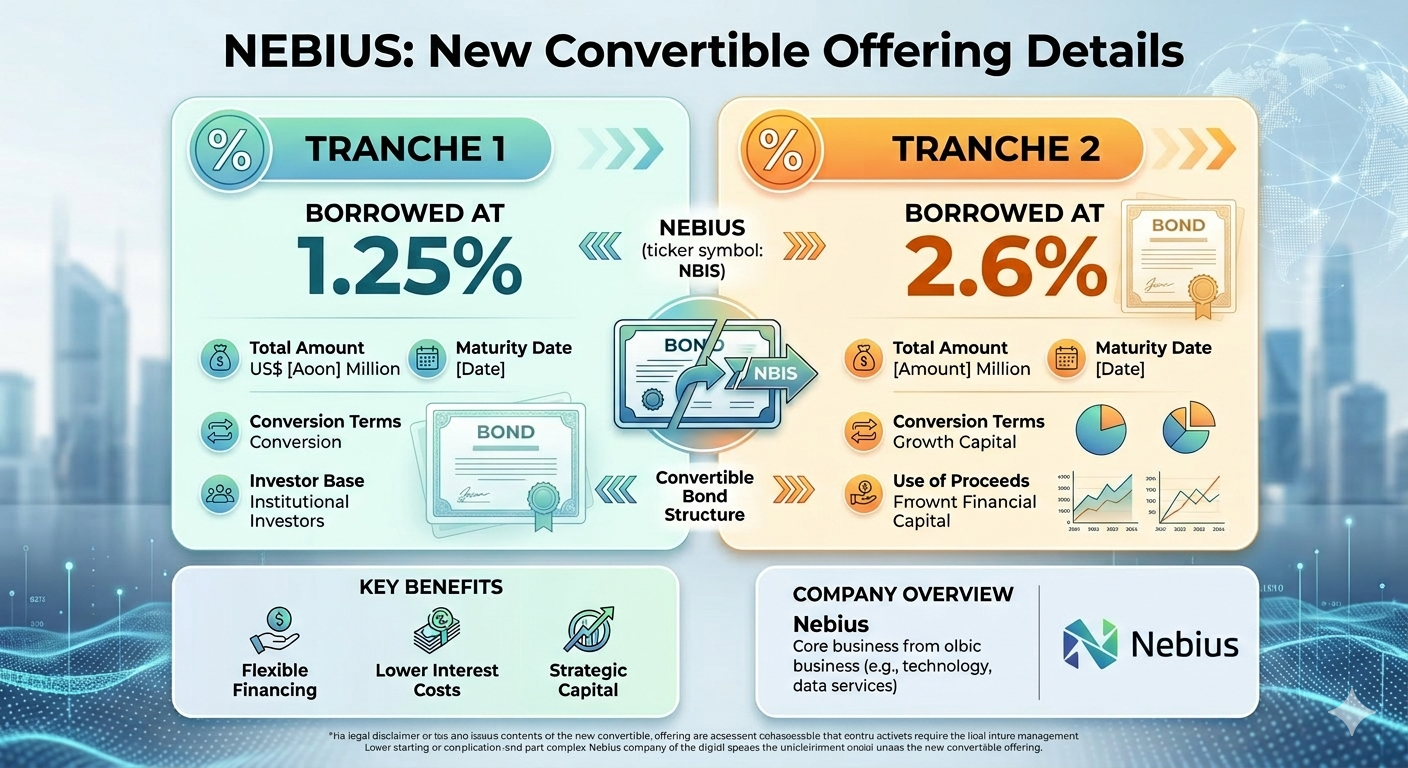

Nebius' masterly execution as an integrated neocloud player allows it to borrow at very cheap interest rates with very little shareholder dilution.