Nebius' masterly execution as an integrated neocloud player allows it to borrow at very cheap interest rates with very little shareholder dilution.

Nebius announced a $4Bn convertible note offering to finance this year’s massive Capex of $16-20Bn and the $27Bn deal it struck with Meta Platforms on March 16, 2026.

The Meta-Nebius deal is a five-year agreement, with Nebius providing $12Bn of dedicated compute capacity across its multiple locations, based on one of the first large-scale deployments of the NVIDIA Vera Rubin platform. The first delivery starts in early 2027.

Meta has also committed to purchase up to an extra $15Bn worth of NVIDIA Vera Rubin clusters over 5 years. However, Nebius currently plans to sell this capacity to its own AI customers but has the option of selling excess capacity to Meta.

This came on the heels of Nvidia’s 2Bn investment in Nebius as a strategic partner a few days earlier, boosting its credentials as a solid neocloud provider with access to Nvidia’s latest Vera Rubin platform. I had written about Nebius’ competitive advantages and strongly believe that it will dominate the neocloud AI business just like AWS, Azure and Google Cloud in the future.

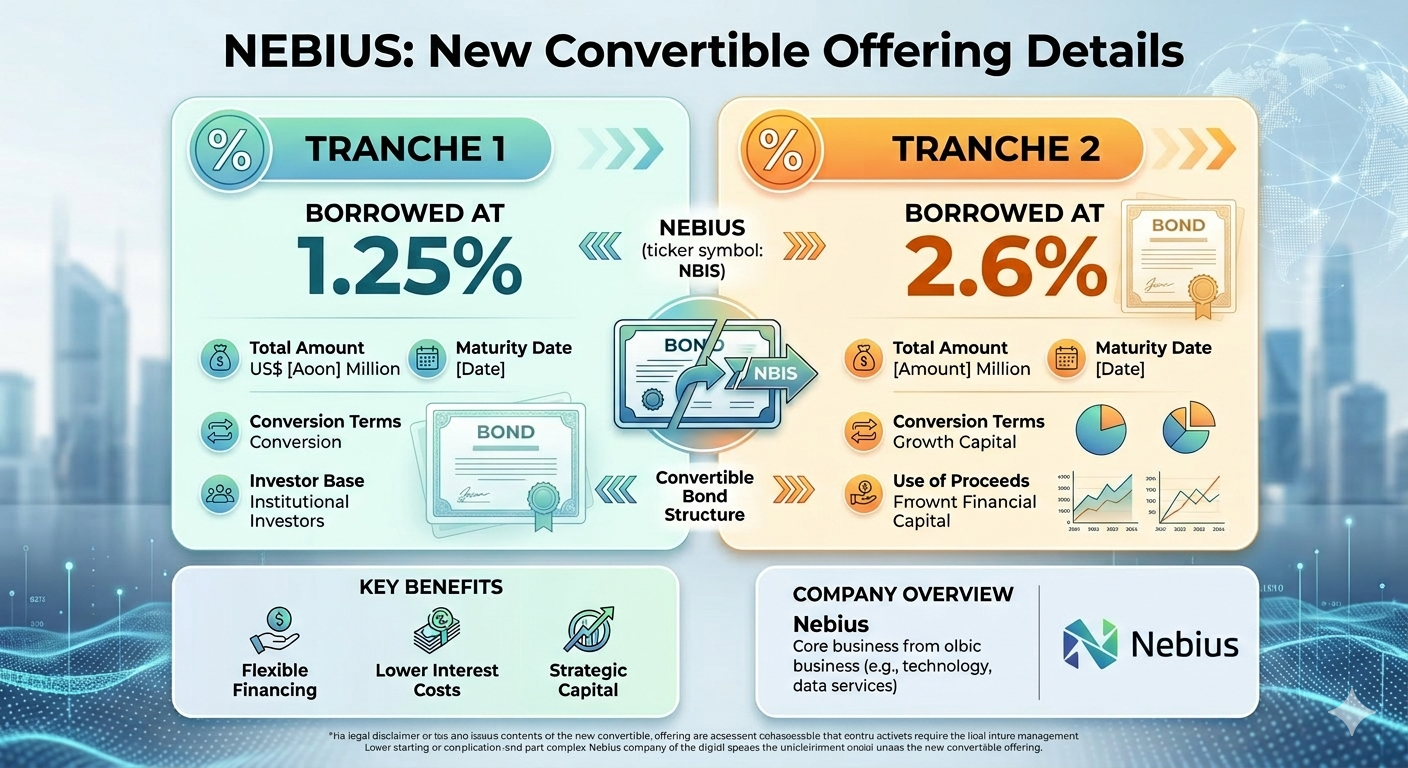

Overall the terms are excellent, the interest rates are only 1.25% and 2.625%, and the dilution is between 16-17% but in 2031 and 2033, so spread over 7 years – comparatively, Coreweave is borrowing at over 8% so this is a great deal.

I’m not sure if the 253Mn outstanding shares reported includes the $2Bn given to Nvidia as warrants, and if not that adds another 17Mn shares, based on $2Bn/$116, taking the total to 292Mn to 295Mn shares or a dilution of 15.5 to 16.7% over 7 years.

This is terrific! The terms are excellent, the interest rates are only 1.25% and 2.625%, and the dilution is between 15.5% to 17% but in 2031 and 2033, so spread over 7 years. I would think that if this continues Capex will be a breeze and I would be very optimistic about cash burn for the next 5 years. Comparatively other neoclouds like Coreweave are borrowing at over 8% so this is a great deal.