There are too many headwinds for the stock market to continue rising, such as a weak job market, and excessive spending from market leaders.

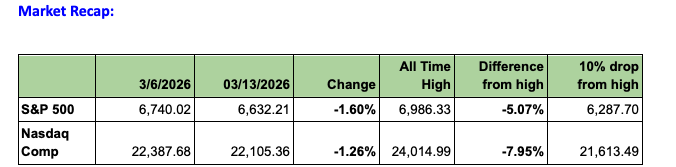

Both the S&P 500 and the Nasdaq Composite lost over 1% during the week. The S&P 500 lost 1.6% and closed 5% lower than its all time high, and the Nasdaq Composite 1.26% but is now almost 8% off its all time high of 24,015, well on its way to correction territory.

Two weeks have passed since the U.S. started its regime change war with Iran and things are looking pretty grim, without a solution in sight. Towards the end of the week I was veering towards a TACO trade, a strategic, face saving exit initiated from the U.S. side, hoping that calmer, cooler minds would prevail. I am not so sure now.

The S&P 500 had one positive day on Monday, up 0.83% when U.S. President Trump tried to talk down oil prices by claiming that the war was almost over, but it was a one day trade as reality hit home with a defiant Iran throttling the Straits of Hormuz.

To briefly recap the war events of the past two weeks; the initial attacks from the U.S. and Israel led to the killing of Ayatollah Khamenei, and a devastation of Iran without 2,000 people dead. Iran on its part has dug in, refusing to U.S. demands of having a hand in choosing its next leader, and instead chose the killed Ayatollah’s son, Mojtaba Khamenei as the next leader of Iran, and in a show of defiance continued to bomb all “supporters” of the U.S. and Israel, pretty much the rest of the middle east and the gulf. It weaponized its only real strength, the Straits of Hormuz, by allowing only Iranian tankers or other ships to pass through it, effectively killing oil and natural gas distribution. As a result the price per gallon of Brent has risen from $78.24 to $98.71 (Saturday, March 14th). Worse, LNG (Liquified Natural Gas) prices for Asia and Europe have jumped about 50% since the war started.

I believe neither side has any real cards to play, the U.S. clearly misjudged the fight left in the Iranians (cheaper drones led the fightback, especially while landing on supposed neutral, non military targets in the Arab world) and it cannot get boots on the ground, so regime change is out of the question. On the Iranian side, the Iranians have nothing besides the Straits of Hormuz; simply, how long can they hold out in the face of two superior armies (in spite of possibly running out of hugely expensive munitions) and a complicit Arab world.

That’s one of the main reasons why I expected an off-ramp face saving exit and continue to do so. I don't believe that a market apocalypse is imminent. I would argue that the IRGC isn’t capable of sustaining this war in perpetuity, but the US can’t sustain the fight either, with the price of gas shooting up to $3.60 at the pump and a stock market that’s falling each week and is well on its way to a correction. The President cares about both. Plus it’s a deeply unpopular war even with Republicans which’ll eventually bleed the sacred stock market cow.

For all the rhetoric emanating from the White House, the options are stark.

Will the U.S. go the scorched - earth route, that is, take the gloves off and target the oil sector and civilian infrastructure or figure an off ramp. There are still two goals from the U.S. side get the uranium’s and change the regime’s. The first cannot be done without taking the gloves off. The second also looks impossible - the hopes of a regime change without organized resistance and a towering opposition figure around whom the public can rally are dismal. And in my opinion, the general tone from the Iranian populace has been to rally against the aggressive Israeli and Americans and sympathy around the world has also seemed to have shifted against the Americans. Simply, the U.S. should have got buy in from the IRGC if it wanted a Delcy (Venezuelan) outcome.

I also don’t believe that the Fed will hike rates, the jump in oil prices is a supply chain one, and not a permanent increase. The fear of rate hikes is irrational.

The 10-year is now yielding 4.26%, with yields rising with the price of oil. The weakness in the stock indices since the war started is eroding the wealth effect and exacerbating the pain from of a huge increase in gas prices, especially when consumer sentiment is at its worst in half a century. I've stressed on numerous occasions that this is a K shaped economy, disproportionately propped up by stock market gains and the subsequent consumption from its spoils, which a drop of 8% indicates that we may run out of the golden goose.

I don’t believe the hawkish read-across from the oil surge for monetary policy would mean central banks tightening (or at least not easing) into a nascent demand crunch, which could in turn tip more dominoes in private credit, resulting in a 2008-style market cataclysm. That would be really, really absurd and a worst case scenario with little ground to support. Ironically, BofA’s Michael Hartnett, who we discussed in the group, actually intimated that this isn’t likely. The financial media has a job to do and we should use our common sense and judgement.

THIS IS WHAT MICHAEL HARTNETT ACTUALLY SUGGESTED AND I QUOTE

“We suggest fading oil >$100/bbl, DXY >100, 30-year UST yield >5%, SPX <6.6k,” Hartnett said, in the same note that contained the 2008 analogue everyone parroted for clicks on

Friday. Those levels, he wrote, are likely “to provoke a policy response that short-circuits Main Street risks.” “Trump can’t allow his approval ratings to fall much further,” Hartnett said, flatly.

Weighing in on the aggressive repricing of US monetary policy expectations, Nomura’s

Charlie Mclligott said that in his view, “very few” clients “actually believe” the Fed will hike this year. I still believe that we will see two cuts, because of the weak job markets.

I had posted a podcast from Mike Wilson a couple of days ago on the WhatsApp groups. He does make a good point about the correction and the logical 10% drop gets us to a support level of 6,300 from the October 31st high of 7,000. There is a 200Day Moving Average of 6,560, which may provide initial support, and if it holds great, but at 6,300 stocks become attractive again. Wilson still has a 7,700 target for 2026, I have not seen any changes in that target yet.

And to his point about higher corrections in individual stocks is spot on.While the index can continue correcting - the S&P 500 is still just 5% off its high, and the Nasdaq Composite 7.9%, a large majority of stocks have corrected significantly higher. Wilson stated that he hadn’t seen so much dispersion between the index and individual stocks in 20 years! For example, a good company like Reddit (RDDT) has corrected 53% from $283. It was massively overpriced but that's overdone. I agree with his prognosis that some money will find its way into beaten down individual stocks.

Reddit (RDDT) $125-$135

Rolls Royce (RYCEY) $16-$16.50,

Bloom Energy (BE) $145-$150,

Figma (FIG) $25-$26,

Vertiv (VRT) $245-250,

Broadcom (AVGO) $320-$330,

One can average the cost down.