The Iran war has driven investor sentiment, but now we are at the finishing line. The worst seems to be over and I believe we should not panic. The S&P 500 is holding its 200 DMA in a steady consolidation pattern.

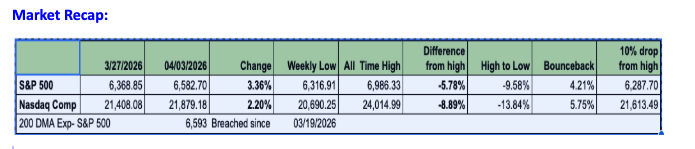

Last week we discussed the S&P 500 breaking its 200 Day Moving Average and heading towards a 10% correction. At that time, the index had fallen 8.8%, and the Nasdaq 11%.

This week both indices fell initially, before storming back on Tuesday with indications that the U.S. would not put boots on the ground and was looking for an exit.

From its low, the S&P 500 has bounced back 4% and the more volatile Nasdaq Comp 5.75%

The volumes for the bounceback caught my attention.

On Tuesday March 31st, the indices rallied very strongly with high volume, optimistic that there wouldn’t be any boots on the ground. The S&P 500 rose 2.9% with a volume of 3.6Bn shares, much higher than its past ten-day average of 3Bn, and followed up with a 0.8% gain on April 1st.

The Nasdaq Composite jumped 3.8% and also followed up with a 1% rise on April 1st. The volumes on the Nasdaq ETF – the QQQ, were at 96Bn much higher than its prior two-week average of 75Bn shares. These volumes indicated sufficient dip-buyers along with short covering and algo traders buying into a declining VIX. (Volatility Index)

I believe the S&P 500 will continue to rally. The S&P 500’s 200DMA is at 6,587, and the index is showing strong signs of holding it in spite of the usual weekend Iran war theatrics.

In my opinion, if the threat of boots on the ground is over, we should see a rally into earnings which start in earnest this week. We can reassess post M-7 earnings, depending on the strength of the rally.

Last week I had hoped that the U.S. and Israel would walk away with considerable wins, such as the decimation of Iran’s air force and conventional military capabilities, the near 90% obliteration of IRGC senior leadership, and its proxies, the enormous damage to its industrial base and thereby its capacity to build advanced ballistic missiles and brought about a kind of regime change. In my opinion, that is the correct strategy. Achieving anything further would have involved at a bare minimum a partial invasion with troops on the ground, even for a specialized limited tactical invasion utilizing a combination of commando raids and Marine landings. It would have been extremely difficult to achieve for limited gains and likely resulted in a quagmire, which this administration should want to avoid. As of now, I believe it has done so. While rhetoric and bluster from both sides could result in more damage, it would be on a smaller scale compared to the previous month. To be sure, oil prices will remain high, and supply chain disruptions won't be solved until the end of the year, but at least we can hope that the worst is over, and the rebuilding process has started.

The Iran war has driven investor sentiment, but now we are at the finishing line.

What conclusions can we draw?

The silver lining: No boots on the ground, no quagmire like Vietnam, Iraq, and Afghanistan for the U.S.; It has achieved several gains as I listed earlier.

What should we worry about?

As of now, Oman and Iran alongwith other mediators will decide on the Straits of Hormuz.