SOFI beat Q3 earnings and revenue estimates handily and also guided higher on the strength of new subscribers indicating solid potential.

SoFi Technologies (SOFI) $26.14

SOFI - Q3 2025 earnings.

SOFI's superb quarter beat on earnings, revenue and guidance: Adjusted net revenue grew 38% YoY to $950Mn resulting in and drove $277M of adjusted EBITDA, which was up 49% YoY. Management boosted full year guidance after adding 905,000 new members in this quarter, for adjusted EPS to $0.37, leapfrogging over the prior $0.31 estimate. It also increased adjusted revenue estimates to $3.54Bn v $3.38B., and adjusted EBITDA guidance to $1.04Bn from $960Mn. SOFI's less risky, capital-light fee-based business was another positive in Q3, with record revenue of $409 million, a diversification that's trending to a$1.6Bn ARR, with a 50% growth rate.

I had first posted on SOFI on 10/07/2025, as an accumulate slowly on declines because of the big 240% jump in the past year, with a likely price target of $32.

Given the solid beat and raised guidance, I would keep the accumulate recommendation.

Here are the details from 10/07/2025 - the analysis remains the same.

SoFi (SOFI) $27.70

It has a lot of positives, but the stock has jumped 240% in the past year.

What are the red flags?

Heavy exposure to unsecured personal loans and intensifying competition from banks and fintechs increase downside risk for SOFI. 50% of revenue comes from lending, with credit exposure.

In addition, its loan portfolio is heavily skewed toward unsecured personal loans, exposing the company to credit cycle and default risks. Meanwhile, larger banks and fintech competitors are aggressively investing in AI-powered platforms, eroding SoFi’s first-mover advantage in the field. Given the inflated expectations and lack of room for error, the stock may be priced for perfection.

Although the management emphasizes that its borrowers have a strong credit profile, with a median income of around $158,000 and a FICO score of around 743, those metrics don’t eliminate the risk of credit losses if the economy slows. In addition, while the loan loss provisions fell in the second quarter, any change in delinquency trend could quickly weigh on profitability. Unlike secured mortgages or student loans, unsecured personal loans expose SoFi to potential volatility in debt write-offs.

The space is competitive with competitors like Upstart, Robinhood, and Chime.

I could accumulate slowly on declines, keeping an eye out on delinquencies or loan loss reserves, especially if the economy weakens.

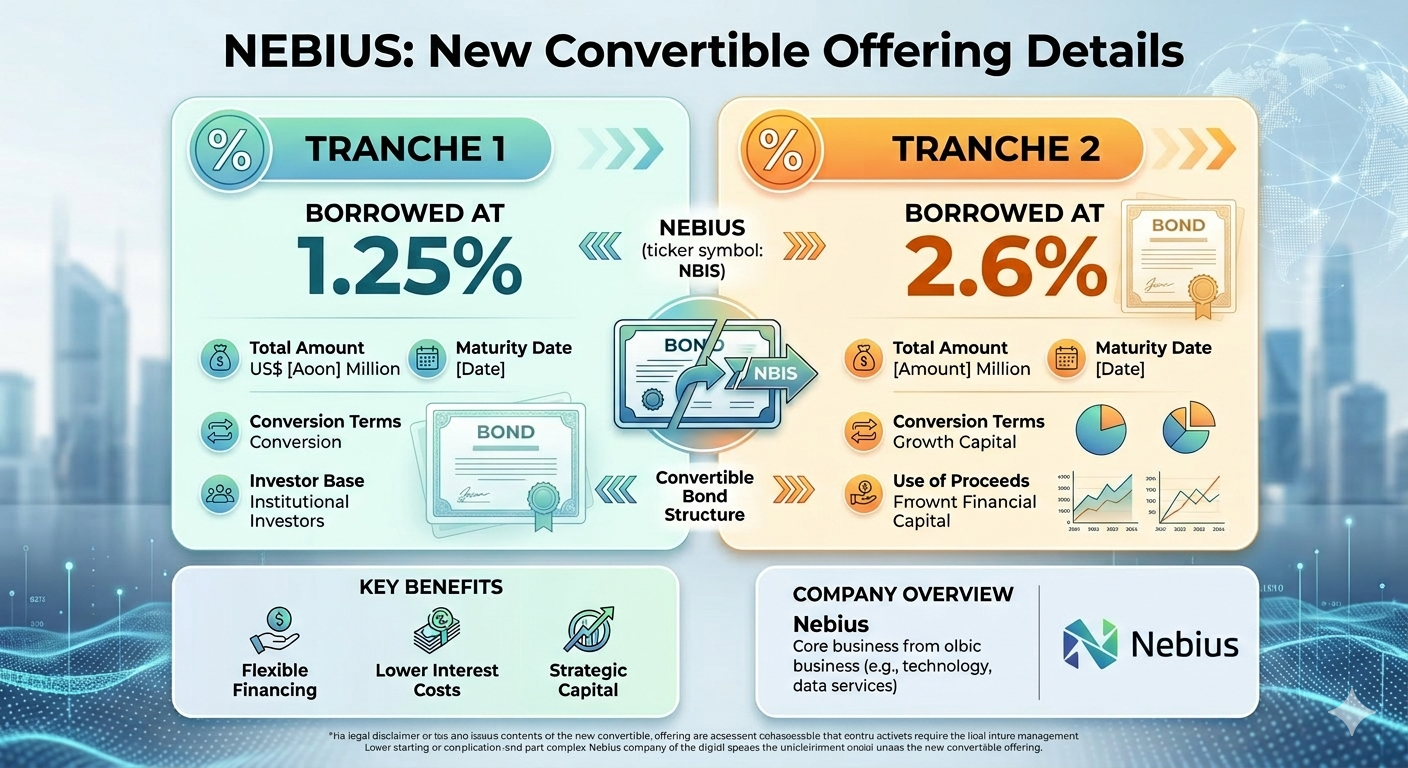

Nebius' masterly execution as an integrated neocloud player allows it to borrow at very cheap interest rates with very little shareholder dilution.