Q3 GDP growth at 3.2%, Nov PCE at 2.8% and a consumer confidence reading of 92 indicate a slow week with less volatility. Stay invested.

Market Outlook - Economic calendar 12.22.2025 - 12.31.2025

The economic calendar is fairly light till the end of the year with just three reports of consequence.

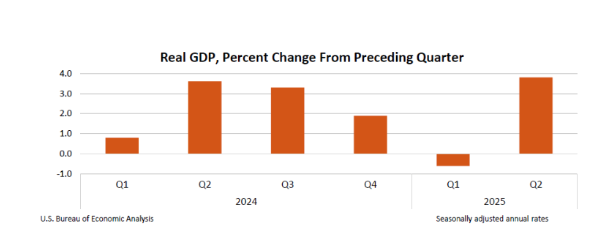

The Preliminary GDP report for Q3 should be out on 12/23, with an estimated growth of 3.2%, a lot lower than the Q2 final growth number of 3.8%. Bear in mind that the last quarter of 2024, and the first two quarters of 2025 have seen several tariff related distortions in quarterly GDP growth, (front-loading imports for example, inventory adjustments) and the estimated 3.2% GDP growth for Q3 should be reflecting some smoothing of what has been a fairly volatile year.

[caption id="attachment_6515" align="alignnone" width="613"] Real_GDP_Growth_2025[/caption]

Real_GDP_Growth_2025[/caption]

A reading of 3.2% is excellent, and should help mitigate and reduce the fear that we’ve seen from discouraging labor numbers in the past few months.

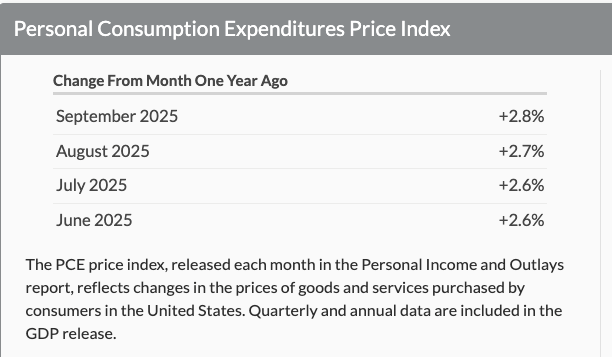

The core PCE (Personal Consumption Expenditures) is also scheduled to be released by the BEA on the same day and at an estimated 2.8% growth is in line with the growth in the past 4 months. There was no release for October because of the government shutdown. The Fed prefers to use the PCE instead of the CPI in their analysis for inflation and even if the report excludes October, it should be of value.

[caption id="attachment_6516" align="alignnone" width="613"] Personal_Consumption_Expenditure[/caption]

Personal_Consumption_Expenditure[/caption]

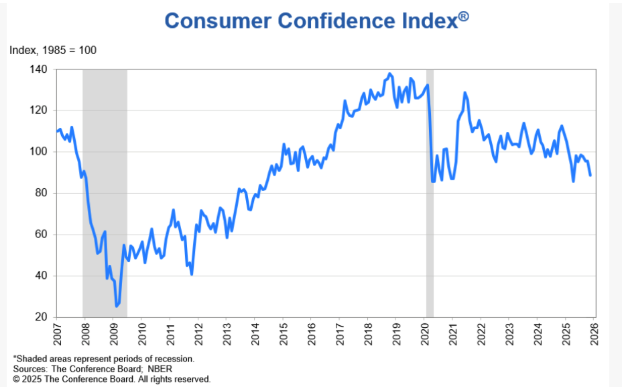

The Conference Board will release the consumer confidence index, which analysts predict at 92, definitely on the lower side and syncing with some of the other softer reports such as the Michigan consumer sentiment survey and PMI readings that we’ve seen in the past few months.

[caption id="attachment_6517" align="alignnone" width="625"] Consumer_Confidence_Index_12.21.2025[/caption]

Consumer_Confidence_Index_12.21.2025[/caption]

Here it is in historical context, continuing to dip, primarily on higher inflation, affordability and the fear of job losses.

These three reports should be mostly benign, continuing the Goldilocks trend we've seen in the past week of neither too hot, nor too hold between a softer labor market and moderating inflation.

As we head into the final seven trading days, volumes will be lower; you're likely to see articles on the "Santa Claus" rally, which traces its roots back to the 1950s suggesting that the last 7 days of the year usually produces an average gain of 1.3%. There is little nuance and context in that observation, and should be ignored.