The consumer confidence report show a harried consumer, racked with inflation, and job losses not seen since the Great Financial Crisis.

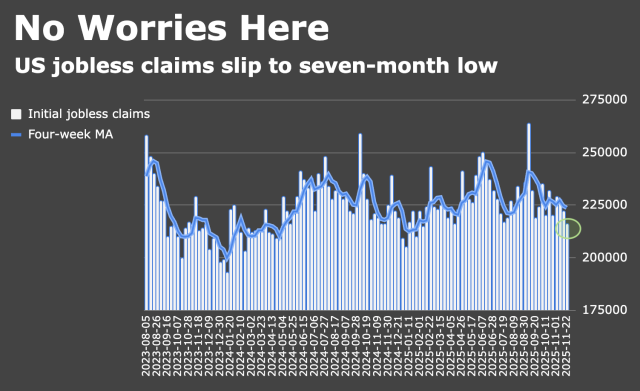

US Jobless claims rolled in at 216,000 for the week ended November 22nd, versus analysts estimates of 225,000, the lowest in 7 months, leading one to wonder what happened to all the layoffs. Continued claims remained high at 1.96Mn , a number last seen in the 2021, before we submerged into an inflation ridden bear market. The continuing claims number of 1.96Mn is a worrying sign, and worse, not showing any notion of coming down.

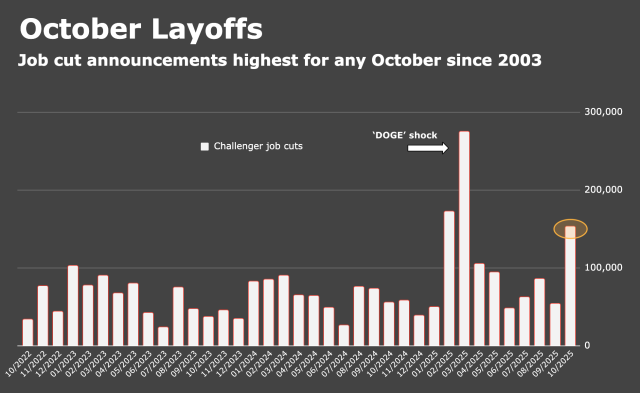

However, the angst from the large layoffs announced by Challenger hasn’t quite made it to higher unemployment claims. In a separate report, two weeks back Challenger had announced a high number of 150,000 layoffs in October, almost 3x its August number. Perhaps presaging an AI induced layoff, which is just peeking out from under the covers.

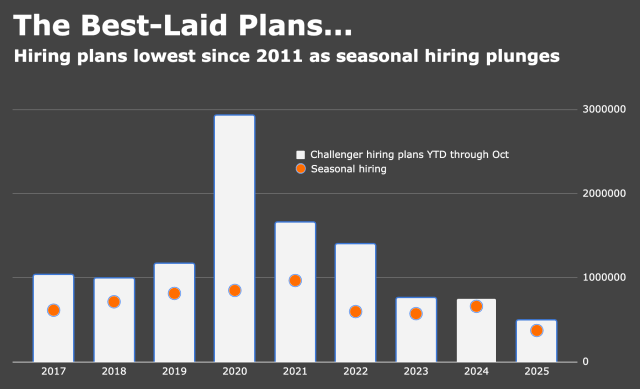

Similarly, Challenger’s hiring numbers also doesn’t bode well for the market with just 488,000 - the lowest in 14 years.

[caption id="attachment_6370" align="alignnone" width="640"] Source:Challenger_TheHeisenberg_Report[/caption]

Source:Challenger_TheHeisenberg_Report[/caption]

What gives? The markets have largely shrugged all of this off since the 11/20/2025 swoon after Nvidia earnings, and have recovered strongly for the past 4 trading days, and we seem to be heading into a likely Santa Claus rally.

On Nov 25th, the Conference Board released it's confidence index and it wasn't pretty. Consumer confidence among US households plunged in November, delivering a very weak reading of the public’s economic mood. The headline index dropped 6.8 points from October to 88.7, marking the second‑largest monthly decline since mid‑2021 and coming in well below the 93.4 level economists expected. Some economists! The index is now at its lowest since April 2025 (Liberation Day) and sits beneath the levels seen around the peak of inflation in 2022. According to Conference Board chief economist Dana Peterson, all major components of the index either deteriorated or stayed soft in November.

It gets worse: The expectations index fell to 63.2, far under the 80 threshold that has often preceded recessions within about a year and close to some of the lowest readings seen since the global financial crisis. Households’ views on future income, job prospects, and business conditions all worsened significantly, with Peterson describing the drop in income expectations as especially sharp and the six‑month outlook for the labor market and business conditions as notably negative. Perhaps this will show up in the unemployment claims, which seem to be lulling the markets into complacency.

This is a surprising development, which makes me wonder if this report is not skewed because of the shutdown. Perhaps the data was collected before the government reopened. Survey details suggest households have turned much more pessimistic in a very short time. In October, a sizable share of respondents anticipated higher incomes in the year ahead, but that group shrank dramatically in November. Very few consumers now describe current business conditions as “good,” and negative characterizations rose sharply.

Open‑ended responses point to a clear list of worries. Consumers continue to cite high prices and inflation as their top concern, followed by tariffs and trade tensions, political conflict, and dysfunction in Washington. Inflation expectations over the next 12 months remain elevated, and many households believe the economy is either in recession already or at risk of slipping into one, even though some broader activity indicators, like GDP growth, have held up.

And the markets keep marching on.....we're up for the last 4 days having recovered 2.5% from the Nov 18th bottom - including a 2.5% drop on Thursday.