A benign Core CPI report with just 2.6% increase in annual inflation Versus estimates 2.7% suggests that price increases are moderating.

There were several tell tale signs of an overdue correction in the past week, and now I believe we are already in the middle of one. The Nasdaq 100 ETF, QQQ peaked on October 29th at 637.01, after which it dipped 8% (during the government shutdown) before resuming its upward journey on Nov 21st, inching slowly to 629.21 in December and then reaching 630 on January 15th, 2026. And now with weight of all our adventures abroad in Iran, Venezuela and now Greenland combined with the fire fighting at home with the Federal Reserve, stubborn inflation, weak job growth we're retreated to 608.06, a good 4% from the high, after making triple tops but not breaking through.

I'm confident that the QQQ will slide to 570, at the bare minimum before consolidating. For the past few weeks I’ve been advising caution in my weekly newsletters, and webinars.

Simply, the large number of exogenous factors had to take its toll, and I believe that the first cracks have appeared in the bond markets, something I highlighted yesterday, when the 10 year closed at a high yield of 4.24%. I strongly believe that we cannot be complacent anymore; even with strong earnings growth of 13-14%, the index is priced to perfection.

These are the reasons why I'm convinced that the next move is lower.

This morning the US bond market dropped with longer maturities leading losses, the US 30-year yields rose 10 basis points to 4.94% and 10-year yields jumped seven basis points to 4.30%, the highest levels since Sept. 3. "

The Japanese bond market is in crisis

Last night, the Japanese debt market cracked, and I’m quoting Bloomberg.

Concern around Japan’s fiscal outlook sent yields on the nation’s 40-year debt rocketing above 4% in the Asian session, the most on record. That’s weighing on long-dated debt around the world, with 30-year bonds also underperforming in Europe.” “Yields on JGBs have reached levels that make investing in US Treasuries unattractive on a currency-hedged basis,” said Ronald Temple, chief market strategist at Lazard Asset Management. “If JGB yields continue to rise, a rational choice by Japanese investors could be to move capital back to Japan.

Treasuries fell throughout the day mirroring Japanese weakness, pushing yields to the highest in more than four months as a fierce selloff in Japanese bonds spilled over into global debt markets. If Japanese 10-year treasuries are offering 2.4% what is left of the carry trade? To invest at home, you need to sell abroad and that's what Japanese traders did.

Thankfully it closed at 4.29%, but I suspect the mayhem could easily continue tomorrow.

The drop was exaggerated, following a US holiday on Monday, with investors reacting to a sea of red in Japanese bonds in the morning on Tuesday, as well as rising tensions between Europe and the US over control of Greenland.

President Trump wants control over Greenland, and is aggressively pursuing it. It at least seems to me, that this is not the usual Trump style take no prisoners bargaining; this is an emboldened President building on his Venezuelan success. The President ratcheted up tariffs to bully NATO countries to handover Greenland to the US. The threat of tariffs, which start with an additional 10% on February 1st, and increase by another 25% on June 1st, could lop off France, Germany, Sweden, Finland, the Netherlands, Denmark and non-European Union members UK and Norway exports by 50%.

What are Europe's options? According to Bloomberg:

They could play hardball The starting point is bolstering the European Parliament’s threat to hold back approval of last year’s trade agreement, which was hailed by Trump’s administration as providing “unprecedented levels of market access” for American products. The deal has not stopped the US from trying to strong arm Brussels into going easy on the tech barons of Silicon Valley and Seattle over regulations and antitrust. There is also scope for retaliation via €93 billion ($108 billion) of potential counter-tariffs on imported US goods, which can serve as leverage in negotiations even if the gloomy market reaction shows it won't be cost-free. There should be an urgent push, too, to unbox the EU’s “bazooka” for the fight ahead: The bloc’s Anti-Coercion Instrument is explicitly designed to defend member states put under tariff pressure by foreign powers. It allows retaliation beyond customs duties, and can potentially restrict market access for titans like Google owner Alphabet Inc. That is a much bigger stick than the usual clobbering of more niche US companies such as Harley-Davidson motorcycles with higher import taxes. French President Emmanuel Macron, still nursing his wounds after failing to stop an EU trade deal with Latin America hated by French farmers, favors this trade weapon — and he’s been backed by German industrial association VDMA. “Europe must not allow itself to be blackmailed,” its president wrote over the weekend.

The European countries to could sell treasuries, they hold a ton, but that would be even worse than a Bazooka. Unfortunately, none of these options will calm markets, and caving could only kick this can down the road, and when does the appeasement stop. I don't believe a European/American split helps markets, handing over Greenland is a green light for handing over Ukraine to Russia and Taiwan to China.

Even with an excellent earnings growth of 13% from $275 in 2025 to 311 in 2026, the S&P 500 sells for 6,770/311 = 22x earnings, way above the 10 year and 5 year averages of 18x and 19x. These prices are ripe for selling and profit taking, the index is priced to perfection.

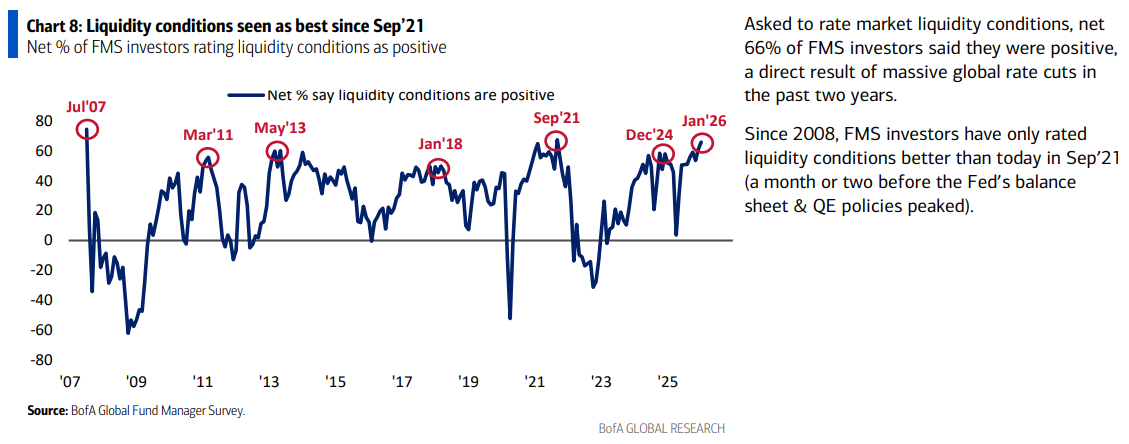

Overbought conditions with fund managers citing the best liquidity conditions since Sep 2021.

[caption id="attachment_6763" align="alignnone" width="1129"] Everybody's a bull now[/caption]

Everybody's a bull now[/caption]

I've sold 7 stocks today, and will continue to sell the rip, I don't see the markets being able to handle the risk appetites of this administration and I also believe that we may reached a point where the US may be the only superpower to be feared but maybe not the trusted ally.

Some of my stop losses are going to be triggered, and I’m also adding put options on the indices as caution. Staying defensive in 2026 is the better strategy, there will be opportunities ahead at lower prices.