Duolingo guided to just mid twenties bookings growth for Q4, with 31% revenue growth suggesting that growth has slowed down.

Duolingo (DUOL)

I had posted on Duolingo's third quarter earnings last week detailed its earnings and guidance.

After the massive 25% drop post earnings to $190-$195, Duolingo has become a bargain, and I bought some this morning.

What went wrong? Duolingo depends heavily on a freemium model , customers get a limited number of freebies and are forced to upgrade to paid subscriptions when they’ve reached the end of their freebies, but this was not resulting a) Daily active user growth and b) conversions to paid subscriptions, and after the initial burst in 2023-2024, bookings plateaued… To correct this Duolingo is focusing on more user participation, giving more time to free users, and investing heavily in product development. This should reignite user growth and bookings by q2, or q3- 2026. The good thing is - even at a paltry $1Bn in sales Duolingo will generate about $370Mn in operating cash this year. Time to put all that cash to use.

The company has realized that in order to get back on the growth track and provide positive returns to shareholders, it does need to take some corrective steps, which will be a little difficult in the near-term, and perhaps will take two to three quarters to bear fruition - the low hanging fruit seems to have been picked. The strategy of going for long term product improvement at the cost of sacrificing margins and profits is the right one.

A bumpy road ahead: The one thing investors need to understand the company has been re-rated, its no longer going to get the kind of high multiple it did, no company gets that when growth slows the way it has from the thirties to the twenties. To be sure, this is not just a revenue growth company, but one with solid profits and outstanding margins. But the risks remain and one should be able to handle a minimum 3-5 year horizon, and also expect volatile quarters such as this one.

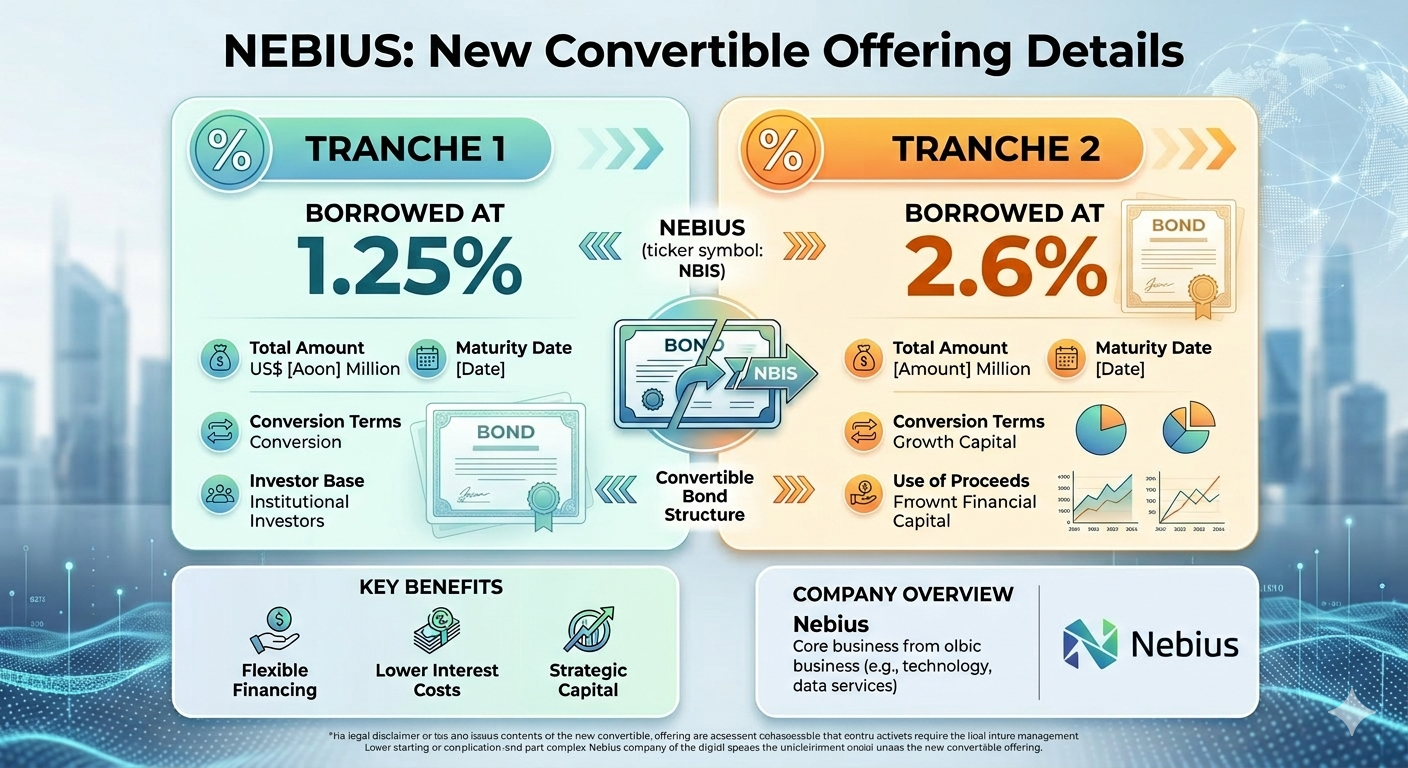

Nebius' masterly execution as an integrated neocloud player allows it to borrow at very cheap interest rates with very little shareholder dilution.

Nebius is executing brilliantly as an integrated neocloud player with tremendous reach, value addition and strong pricing power.