There are too many headwinds for the stock market to continue rising, such as a weak job market, and excessive spending from market leaders.

In my previous newsletters sent to premium subscriber and in the webinars, I have been wary of a long overdue correction of 10%, and that the stock market alone couldn't sustain the economy. Simply weak jobs growth after all those massive downward revisions suggested a weakening, and worsening economy, reliant on a consumer that simply is running out of the wherewithal to keep spending. How much can the stock market sustain the economy? Now that the Nasdaq Composite has fallen over 5% from its 2025, Oct high of 24,019.99, I believe that the Nasdaq composite would correct 10% to 21,613, and the S&P 500 to 6,288.

Among other reasons, I had cited the following:

The markets topping out and unable to scale new highs.

The inability of the M-7 to go higher because of a re-rating of multiples due to high Capex.

The rotation into small caps, industrials and other sectors, which didn’t carry enough weight in the indices.

The weak and steadily weakening labor market, which is terrible for a consumer driven economy.

AI undermining SaaS and enterprise software companies.

A weak housing market.

Stubborn inflation and high budget deficits making it difficult to cut rates.

A weakening crypto currency market getting squeezed by credit markets that could drag the entire equities market with it.

Maybe I was wrong in calling for a correction, or too early but I just don't believe that we can get back into stocks unless there are some compelling values. After recovering on 02/06 - Friday, when crypto bounced back, there was some follow up buying on Monday, 9th February.

But after that we've had four down days in a row, and leadership has collapsed. By that, I mean the $650Bn of Capex is going to weigh down leaders like Amazon, Microsoft, Meta and Alphabet. Tesla is a wild card, leaving only Apple and Nvidia to carry the M-7. So that math is simple, if 35% of the index has either topped out and remains stagnant the balance 65% has to work twice as hard to keep the index moving.

And a decent chunk of the index is in two sectors that are stuck as well, enterprise software and housing. Housing is supposed to be 15-18% of the economy. Enterprise software, which is part of the broader digital economy contributed $4.9Tr in 2025 to US GDP or about 18%. The digital economy was also responsible for 29Mn jobs. Gartner estimates that software spending for 2026 will total $1.4Tr, about 5% of US GDP. I don't believe the broader economy can be immune from pressure from these two large segments.

We've seen sector rotation for the past 3 months and I believe it will continue, but small-caps cannot carry the index.

Last week I wrote about the surprising payrolls gain for January of 130,000 net jobs, albeit juxtaposed with massive revisions, reducing 2025's total gains to just 181,000 jobs or 15,000 a month. Goldman Sachs feels the same way, it cites weak payroll as the biggest risk, the weak job growth exposes the soft underbelly of the US economy, which is showing a few cracks.

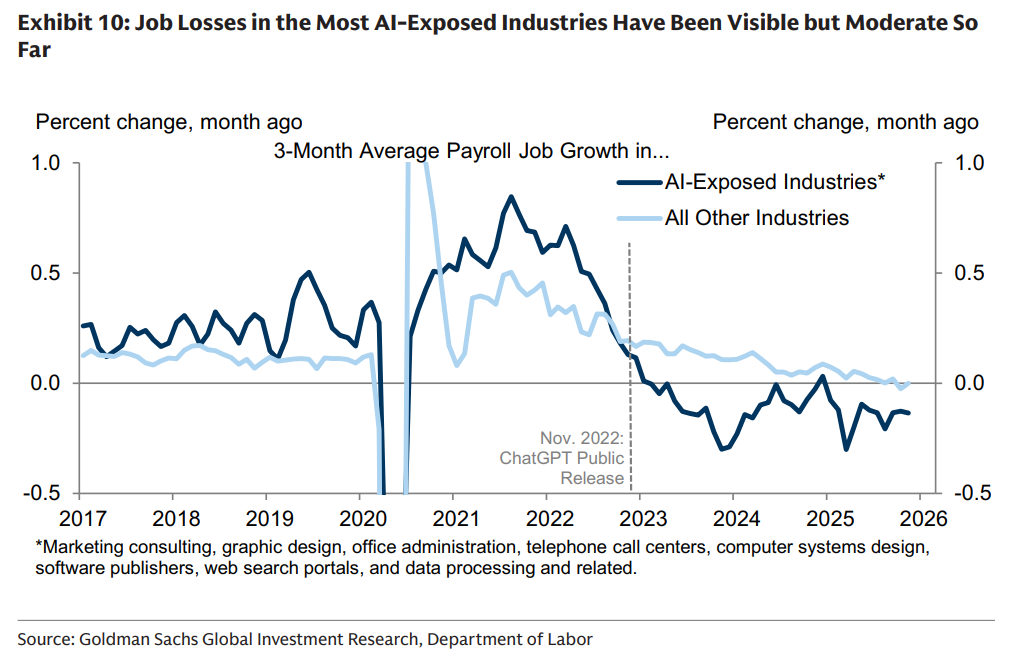

The key risk for the U.S. economy continues to be a labor market forecast that is “tilted towards a worse outcome,” according to David Mericle, chief U.S. economist at Goldman Sachs. The economist said the starting point for labor demand “has not looked very healthy,” with job growth weak and narrow, hiring rates very low, and job openings “too low and still appear to be trending lower.” Mericle also expressed concern that payroll growth “has been very narrowly confined to the healthcare industry,” which was less troubling when it first emerged in late 2023 but is more concerning now that jobs-workers gaps in several industries have fallen below 2019 levels.The main reason for the downside risk, he said, is “the possibility of a faster and more disruptive deployment of artificial intelligence.”

Job growth has turned slightly negative in subindustries where AI is most ready to deploy, with the strategist estimating that “job losses in these areas have amounted to a 5-10k hit to overall job growth.”

Job Losses in the Most AI-Exposed Industries (Goldman Sachs Global Investment Research, Department of Labor)

Key takeaway: I believe that unless job growth starts turning around, and interest rates are lowered we could be headed for a very difficult 2026; the multitude of headwinds should result in a correction of 10% in the S&P 500 to 6,228.

Portfolio and investment strategy: Increase risk mitigation and raise the bar for investing with strict limits to keep a minimum margin of safety of 20%.