UnitedHealth has started the long and painful ride back to recovery with a small earnings beat and higher guidance by reducing medical costs.

10.28.2025 Sep Q3 - Earnings Update

UnitedHealth (UNH): Modest Improvements Spell Hope and Limited Downside

Earnings beat - Q3 Non-GAAP EPS of $2.92 beats by $0.11, but still 50% below last year. The quarter that shook United's foundation.

Revenue of $113.2B (+12.3% Y/Y) beats by $140M. The 12% revenue growth is a great sign - United messed up on high morbidity and uncontrolled expenses, but at least sales keeps growing making an earnings bounce back feasible.

The medical care ratio (MCR) of 89.9% was in line with expectations, but bear in mind, United's MCR has been around the low eighties so there is a lot of work to do here.

Operating cost ratio of 13.5% - not terrible again and can be a springboard for the future.

Segments

UnitedHealthcare revenues, its biggest segment grew faster than the company at 16% to $87.1Bn, helped by Medicare & Retirement and Community & State growth.

And it wasn't just the total, they added 795,000 new customers in the past year, reaching 50.1Mn consumers.

Optum, was a weaker segment, its revenues grew less at 8% year-over-year to $69.2 billion, driven by growth in Optum Rx.

(United has inter-company eliminations of $44Bn between Optum and UnitedHealthcare)

Days claims payable of 46.2 compared to 44.5 in the second quarter 2025 and 47.4 in third quarter 2024.

Guidance

It raised 2025 GAAP earnings outlook to at least $14.90 Per Share; Adjusted Earnings of at least $16.25 Per Share vs $16.22 consensus. Consensus analysts forecast a range of $16 to $22 for 2025, 41% below the previous year at mid-point, and a small growth of 10% for 2026, to about $18. The stock has jumped from a low of $240 - a 50% gain after investors decided a bottom was in. I suspect it will consolidate at these levels, before another leg up.

Crucially, it cannot have a bad quarter, they've just begun to regain their credibility. In their favor is a relatively low multiple of just 20x earnings - far below the historic 30x average. United insures 50Mn people, and is the largest insurer by far, and more often that not, its premium is justified,

We own it and will continue to hold it for the foreseeable future.

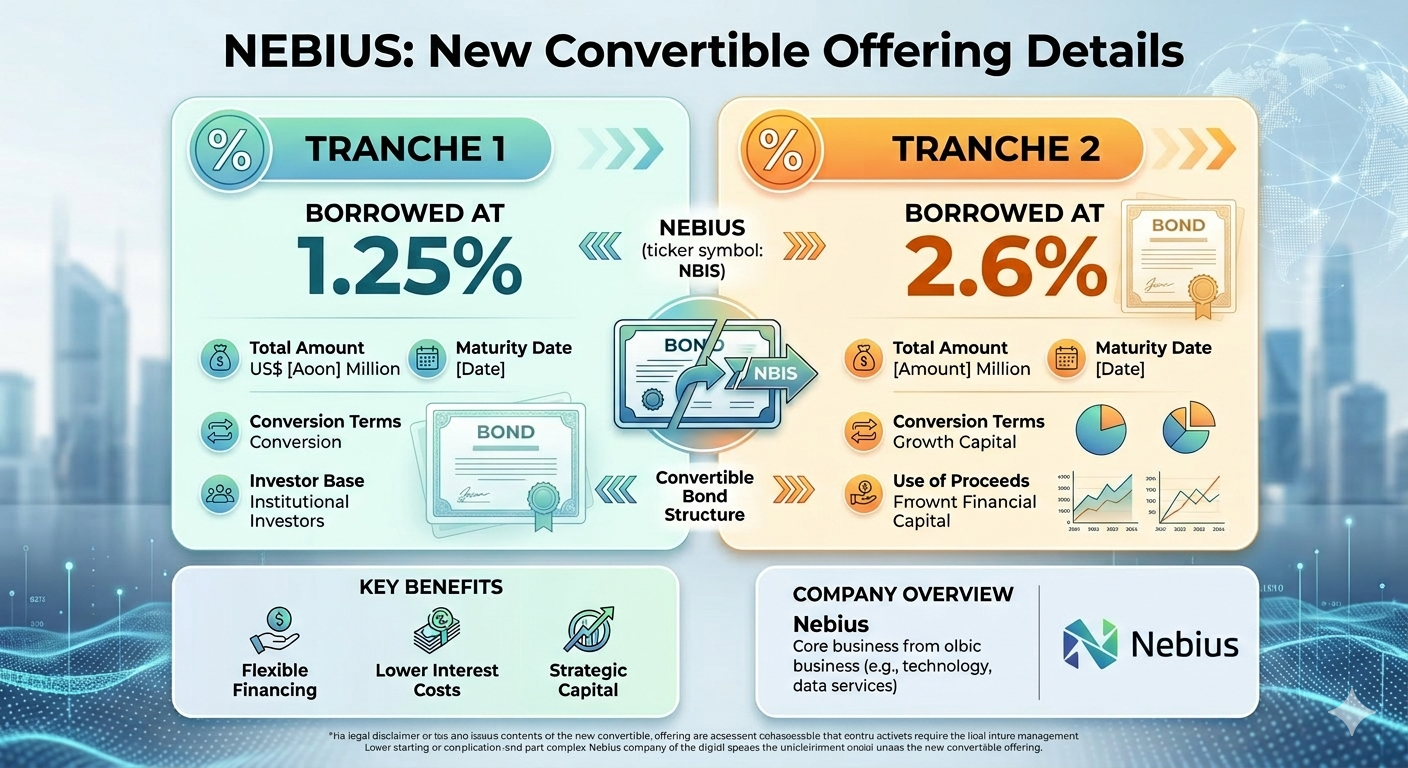

Nebius' masterly execution as an integrated neocloud player allows it to borrow at very cheap interest rates with very little shareholder dilution.