Boston Scientific and Abott Labs offer steady, sustainable, and recurring revenue streams and are worth buying for 10-12% annual returns

The sustainable medical device industry

The medical device industry has been a steady performer in the past decade - this business offers steady sustainable and recurring revenue growth and some operating leverage for earnings to grow faster.

The medical devices sector is a mature sector with the following metrics:

PEG (Price Earnings to Growth) ratios of 2.06 to 2.6, which is the correct valuation to use for such a wide range, except for Intuitive Surgical, an outlier at 4.16, commanding a multiple of 59 with just 14% earnings growth. The PEG of around 2 is reasonable given the long history of sustained and recurring sales and income.

The industry obviously has legs, all companies have had decades of steady growth, and as far as analysts can project this growth is likely to extend for another decade.

The key question then is to find a single bargain that can outperform?

I think Boston Scientific, (BSX) has the best chance of outperforming from both a valuation perspective and from a product/competitive positioning point of view.

Biggest catalyst for these stocks - Beating steady growth forecasts with margin improvements or improved product lines, which point towards BSX as the leading contender in this bunch.

Given our strategy to look for more steady, defensive plays with limited downsides, the recurring nature of these businesses is very appealing.

Boston Scientific BSX $96

BSX - Boston Scientific's forecasted to grow sales and earnings 11 and 14% respectively annually for the next three years, continues to deliver robust growth. It also has market leadership in some of its product categories.

Currently it has two major growth drivers—Farapulse (PFA), and Watchman (LAAC), with several other catalysts increasing its pipeline. There are growth opportunities in interventional therapies, and neuromodulation as well through 2028.

Boston Scientific has targeted over 10% annual revenue growth and for the most part has met estimates. With an operating profit margin of 18% and cash flow margin of 21%, there is excellent operating leverage, and earnings are forecast to grow faster at 14%. For the past decade, BSX has grown revenues at about 8-9% and its laudable that it continues to grow even faster on a higher $20Bn revenue base. Management presented at its recent investor day for multiple years of over 10% revenue growth with 50 to 100 basis point increases in margins, and I believe it will achieve them.

Challenges - Not meeting targets or heightened expectations - the street could expect 11%-12% and lower guidance may disappoint investors.

I don't believe valuation are stretched - BSX is pretty much at the sector's valuation and with a PEG of 2.1, and a P/S to Growth ratio of 0.6, BSX is right in the middle. I do find it difficult to argue for meaningful undervaluation, but that's acceptable, I don't have very high targets and would sacrifice high returns for less volatility. In the worst case scenario the stock could remain rangebound, but I will accumulate on declines - this sector is very, very interesting and offers stability in an expensive market.

Medtronics (MDT) $97

As the second largest company it has been the slowest grower, but also offers a dividend yield of 3%, which is a plus given the steady nature of the business and those seeking a solid dividend yield or income. Medtronics is among the largest with a strong presence in 150 countries and most diversified medical-device companies in the world, with a stable of cardiovascular, diabetes, neuroscience, and medical-surgical therapies for over 70 health conditions. Its strengths include minimally-invasive robotics and closed-loop diabetes systems.

Beating estimates: MDT jumped to a higher revenue growth trajectory after several quarters of deliberate investment, borne by surging growth across key verticals during fiscal Q2 2026 . Revenue grew 6.6% YoY, including 5.5% organic growth, 75 basis points above the midpoint of management’s guidance, which is a lot higher than its decades long 3% growth. Another bright spot was its adjusted EPS growth of 8% YoY during fiscal Q2, beating management’s previous guidance.

MDT's dividend yield is a strong 3% and the higher growth prospects have already earned the stock 21% this year. The stability, and scale are attractive, but might be already reflected in the price and I could look at it again on declines.

My biggest challenge with Medtronic would be the lack of growth - we could be stuck in a value trap, but given the recent improvements I want to revisit this company again.

Stryker (SYK) $352

Stryker's also showing some mobility like Medtronics, delivering strong growth of 10%, higher than its three year outlook of 8%.

Still it bought growth with the $4.9Bn Inari Medical acquisition this year to boost its neurovascular business. The debt for the acquisition, naturally increased leverage, but Stryker's cash flow generation from higher revenues should get it back on track to reduce leverage soon.

Valuation multiples are not that high 24x earnings with a PEG of 2.2, close to historic valuations, and if it surprises to the upside, SYK could return over 10% as well.

The dividend yield is poor at just 0.9%, and there’s not much in terms of the story making it a hold.

It could become interesting on a pullback.

Abbott Labs (ABT) $125

Abbott Laboratories is solid, with a stronger dividend yield of 2%. Like the others it has robust fundamentals, and operational leverage. I'm also impressed that it can grow 8% at its humongous size of $45Bn.

In its last quarter, ABT delivered double-digit EPS growth, also above its historical norm, and from both medical devices and its other products. It increased its dividend by 7%,

Abbot's pending acquisition of Exact Sciences for $21Bn should be accretive next year. I would like to keep an eye out for synergies from this acquisition - their portfolios will complement each other. I'm not planning to add at this price, there's not much room for error given the Exact Sciences roll up - but the valuation looks interesting in the event of a 15% pullback.

Intuitive (ISRG) $574

Intuitive Surgical is priced to perfection at 59x forward earnings and even with robust Q3 results, of 23% revenue growth and big beats on EPS and revenue, seems like chasing an overpriced stock, with a 40% increase in the past year. There's little room for error, and no margin of safety.

ISRG's premium valuation is well deserved but not as much as 3x over the sector, which prohibits entry till there is a pullback. It also seems that they have learnt the art of sandbagging to perfection. There is competition as well from Medtronic's Hugo platform.

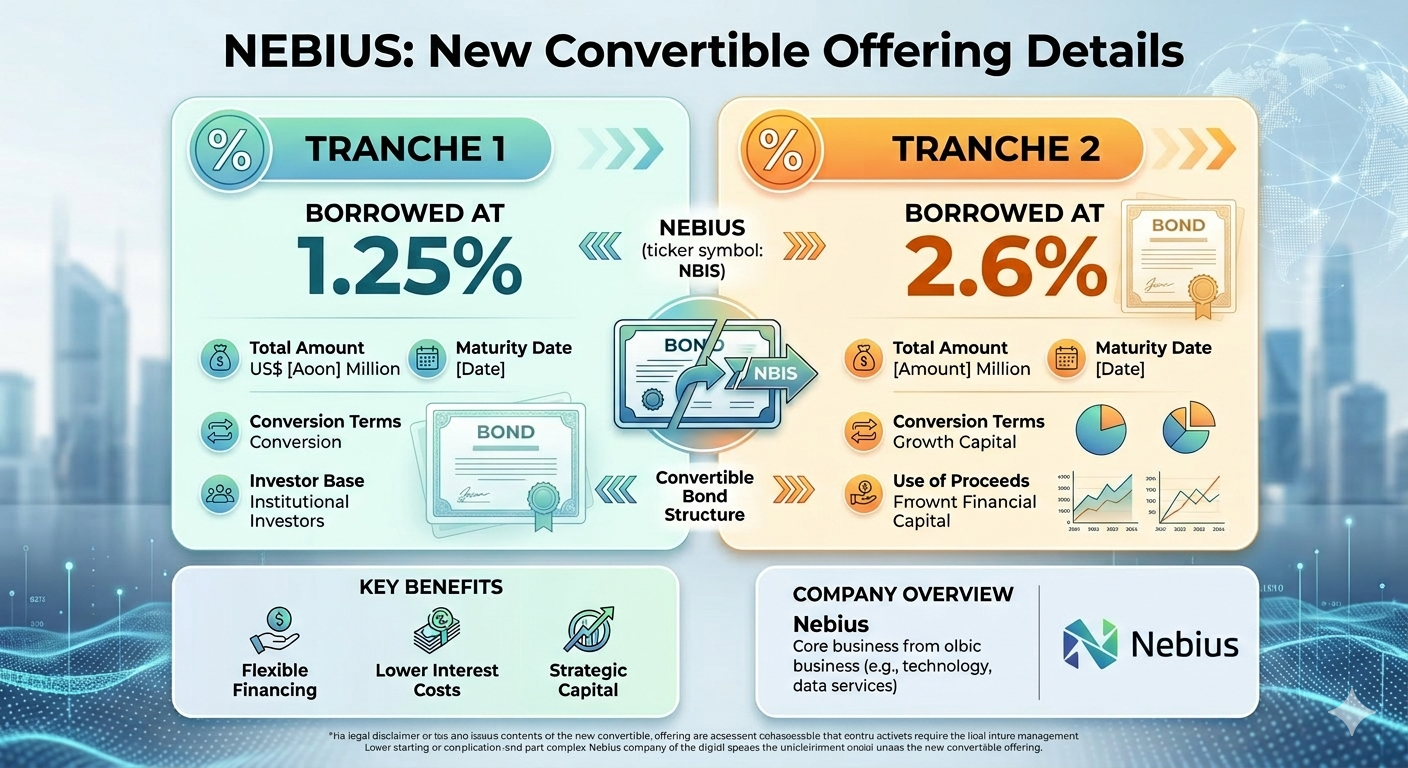

Nebius' masterly execution as an integrated neocloud player allows it to borrow at very cheap interest rates with very little shareholder dilution.