The high-flying Intuit, a market leader in small business accounting, payroll and tax has fallen 50% from its high to a reasonable valuation.

Strong, market leading products: Intuit (INTU) is a rock-solid company with strong fundamentals and sticky clients for several of its products such as Quickbooks (80% market share of small business accounting) and Turbo Tax.

Tax law changes: The One Big Beautiful Bill should help Intuit's tax business grow.

AI additions: Intuit has added AI capabilities across its product dashboard.

Bundled services: Intuit has a vast ecosystem of tax, accounting, payroll, credit card processing, loans and credit.

Improving valuation: INTU finally trades at 17x FY26 P/E and 14x FY27 P/E, with earnings growing 14-16% with a PEG ratio near 1.2x, signaling a reasonable multiple to growth. Sales, too, are expected to grow at a reasonable clip at 12-13% per year. The business remain excellent.

Valuation: Intuit’s biggest problem had always been its valuation, it was rare to see it below 30x earning close to a PEG of 2. Now, however with AI knocking the wind out of its sails, Intuit trades at near fair value.

Competition: The big weakness I see is increased competition and the likely loss of pricing power. Simply, the greed of price increases in the last few years had led to a lot of unhappy clients looking for cheaper alternatives, but for the most part Intuit managed to retain and grow because most alternatives were not intuitively easy to use - not worth the change. For most folks who used Quickbooks, the simplicity of the system had always been its strongest asset. The big mistake that Intuit made was they started overcharging to a point where it became prohibitive for small businesses, its biggest market.

That said this is finally at a reasonable valuation, but competition from foundational models providing generative AI APIs and upstarts using their AI tools to disrupt Intuit’s SaaS model will ensure that pricing will remain in check - thus investors shouldn’t expect too much from it, and be on the lookout for lower growth inflection points.

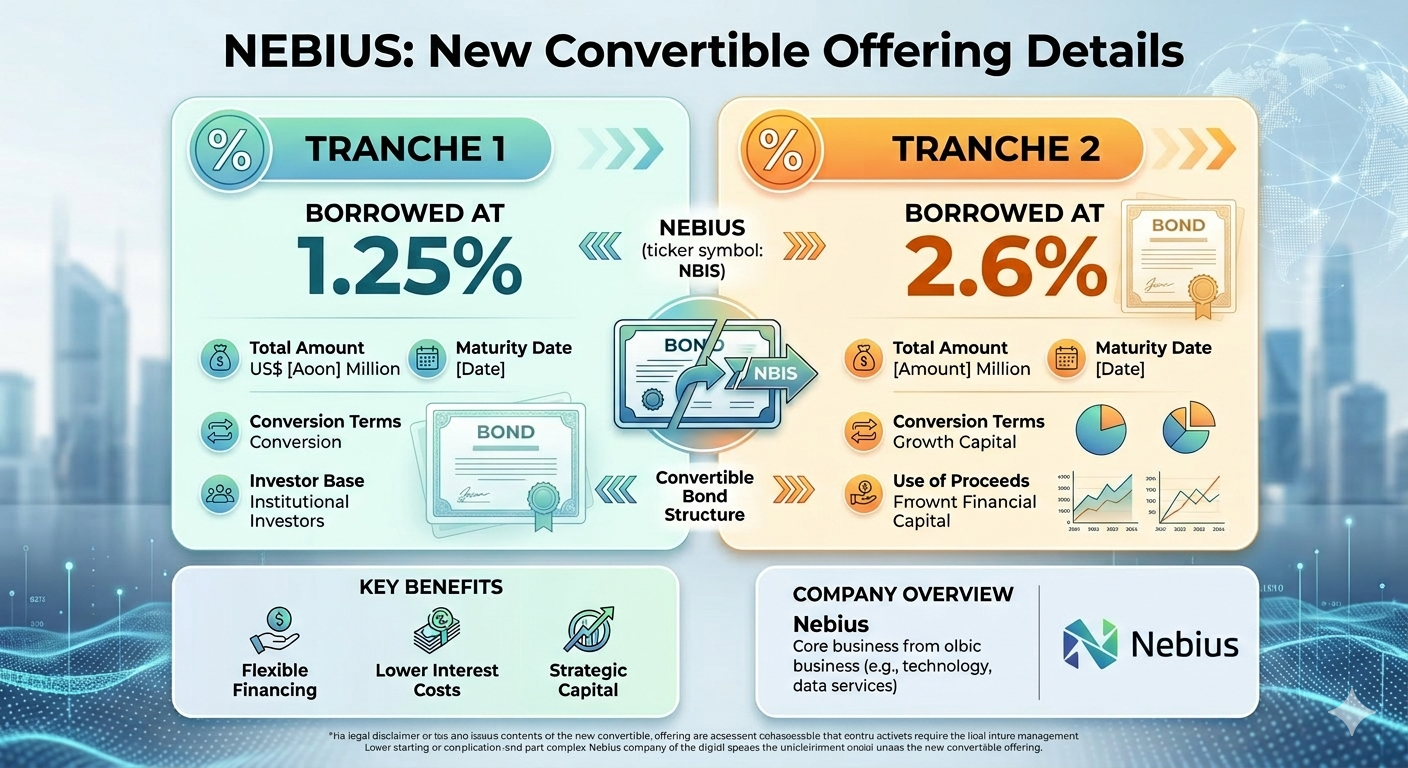

Nebius' masterly execution as an integrated neocloud player allows it to borrow at very cheap interest rates with very little shareholder dilution.