Goldman's Sachs is the market leader in M&A and in its wealth management business, and worth buying in declines.

I like Goldman, it is one of the best in its financial sector, with strong market leadership positions in its segments; but after the 65% gain the past year, way better than its usual return of 17% a year over the last 10 years, I am hesitant to buy unless it declines. Earnings are projected to grow around 14% and its valuation is at the high of its range at 17 - so no bargain for sure.

There will be a lot of strategic points to consider, and I don’t plan to do anything prior.

For the 4th quarter, analysts expect an adjusted EPS of $11.71 and revenue of $14.26Bn. Besides EPS and rev growth, the quality of earnings would be a more important metric. It would show that Goldman’s earnings have become more stable.

AWM net inflows, and double digit growth in fee income are key and higher revenue from advisory and financing, would show Goldman still leads in M&A and deals.

Goldman should also show operating leverage with better operating margins.

I would be on the lookout for a slow down in business should there be weaker, sequential fee growth. Higher buybacks and dividends would signal confidence about future profits. JP Morgan didn’t signal weakness with higher provisioning, at least not more than usual, and Goldman’s provision should be interesting.

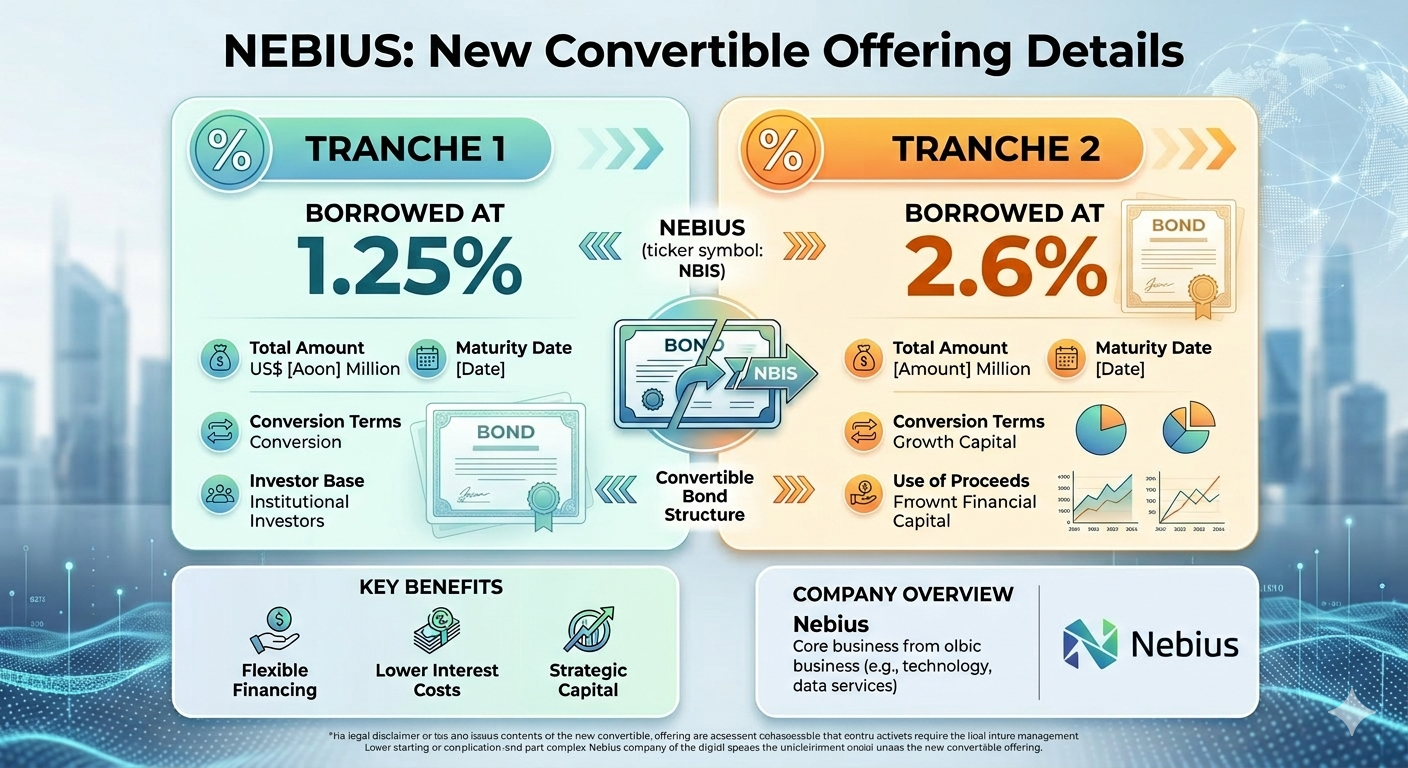

Nebius' masterly execution as an integrated neocloud player allows it to borrow at very cheap interest rates with very little shareholder dilution.