Private lending has a lot of exposure to SaaS and data center infrastructure companies, and it has redemption problems. Investors should remain cautious.

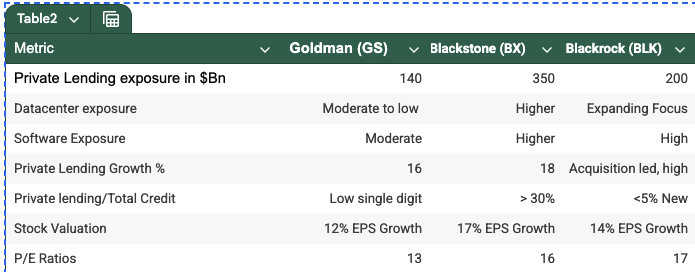

A subscriber asked about investing in beaten down private equity lenders, Goldman Sachs (GS) $810, Blackstone (BX) $110 and Blackrock (BLK) $953.

Overall, I would be wary of investing in private credit related stocks for a bit, and would need to see their stocks fall even more for a higher margin of safety but among the three, Goldman is relatively less risky of the three, and the stock is down 20% from its 52 week high.

Redemption issues

BlackRock capped at the 5% quarterly limit on March 6th, not a good sign, because it’s a major.

Blackstone also had problems and raised the gate to 7% last week.

The default rates tend to be as high as 5% for private lending with some indications of 9% so this is a fairly high yield/high risk sector.

I would avoid Blackstone because both software (SaaS) and data center related exposure is too high. Blackstone has dropped almost 50% from its 52-week high and looks tempting but I’m not convinced yet.

I would avoid Blackrock, because it’s late to this sector and as a result is over compensating and is too aggressive. It has dropped almost 30% from its 52-week high but still needs more margin of safety.

I don't own Goldman but if one had to choose a beaten down private lender, it would be Goldman Sachs around $750 with an ample margin of safety.