The high-flying Figma, an Adobe killer has fallen 75% from its high to a reasonable valuation. Buy the stock.

Industry/Sector/Type - Software, SaaS/The industry going through massive re-rating

Biggest catalysts for the stock - Positive: Product acceptance and growth in the design/creative space. Negative: Vibe coding products would cut margins and pricing.

I like the company and it is a cautious buy around these levels and more on declines.

Following its IPO, Figma soared to over $140s as investors bought the Adobe killer and "Google Docs moment" for UI/UX design ( the collaboration layer for app design teams). The bullishness was founded on Figma expanding its offerings wider into virtual workspaces, documents, websites and other products for tech development, white-boarding and design for software applications. Products like FigJam, Figma Slides, Figma Make and Figma Buzz started gaining acceptance, however it soon became wildly overpriced at over 25x sales and 200x earnings. And then Anthropic happened, eventually leading to SaaSmageddon and panic, besides the inevitable downgrades.

Negatives:

While there is a lot to like about Figma, the SaaSmageddon fear will likely persist till there is an acceptance or a change in the "SaaSmageddan"narrative.

It will cap multiples and Figma is already at 9x sales and over 100x current earnings. It needs to improve its bottom line fast. It is cash flow positive but at only 14% of sales.

Figma’s needs to improve operating margins higher, because with competition from amateur Vibe coders will hurt pricing. It hasn't quite figured out that piece of the puzzle yet.

Reduced barriers to entry and increased competition in the software space has surged and will continue to surge in the mid to long term, which means that the growth rates of these companies could decrease drastically. However, building a tool is just 8-12% of total costs, even the tiny Figma has 80% gross margins; there are distribution, marketing, and user acquisition costs. I don't believe that startups using pure vibe coding tools can survive getting to market. Most SaaS will fail before getting to market. Besides coding there are significant barriers to entry, and I don't see that reducing anytime soon.

Figma's resilience and strong earnings is a good shot in the arm for the broader software industry. Besides it is at a very attractive entry point, with a limited downside. Further sales growth projections have whittled to just over 20%, which ironically could translate into positive earnings surprises in the future.

There is little downside risk at this price and a good margin of safety. I will continue to add in tranches

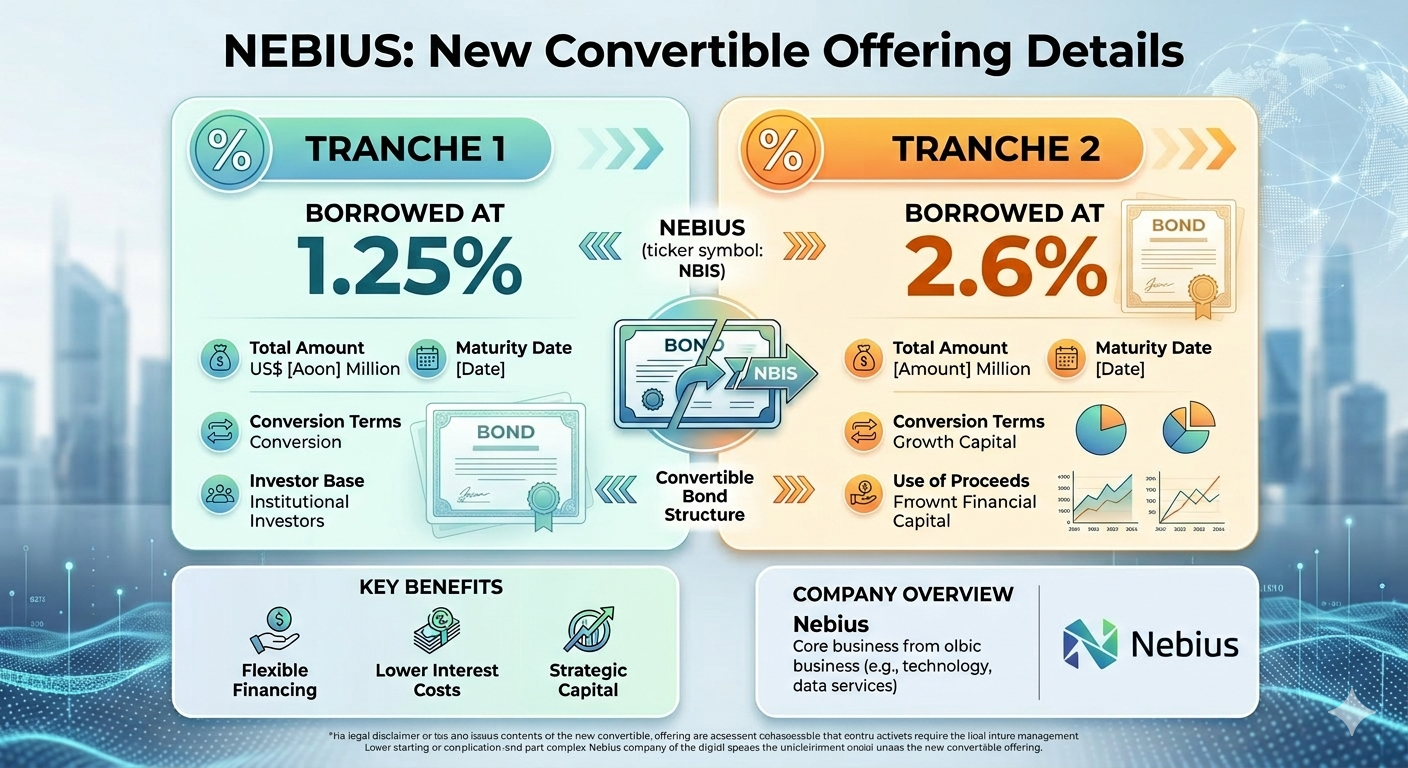

Nebius' masterly execution as an integrated neocloud player allows it to borrow at very cheap interest rates with very little shareholder dilution.