DoorDash's quarterly results confirm my buy recommendation as a long-term investment, which will earn investors tremendous rewards in 27-28.

Two days back I had published an article reiterating a buy for DoorDash, around $160, stating that the sell off was overdone. DoorDash reported post market today and after an initial hesitant drop roared back on some very impressive volume growth. I believe that a) the combined sales increase of 38% after merging Deliveroo and b) management assurance of improving long-term margins are reassuring signs that DASH has bottomed out and its share price would only move higher from here.

Here are the details from their press release.

Fourth Quarter 2025 Key Financial Metrics include Deliveroo numbers as the acquisition was completed in Q4-2025

Besides, top line and volume growth, DASH is becoming an earnings story Covid -19 influenced revenue growth at all costs, and I believe investors will reward it with higher multiples in the next 2-3 years.

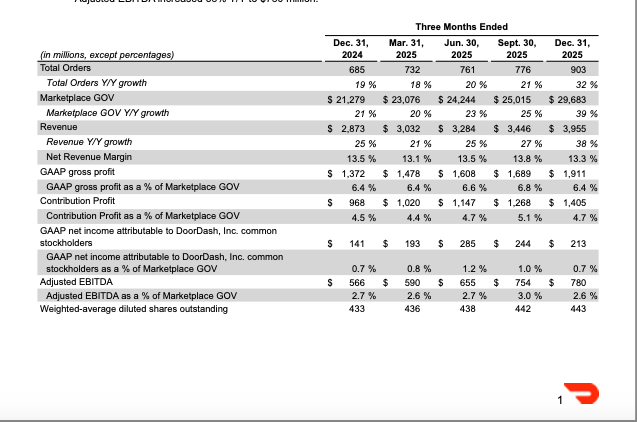

Here are the company's detailed quarterly operating metrics.

In 2025, DoorDash exited the year with over 56Mn monthly active users (MAUs) and over 35 million DashPass, Wolt+, and Deliveroo Plus members. The DashPass, Wolt+ and Deliveroo Plus cohorts are the premium cohorts an having 35Mn is fairly sizable.

I believe Dash's success lies on its loyalty, and the wider reach of its platform, it will attract new users and increase volume from existing users who see this as a best way to order anything in food and groceries, a sort of a ubiquitous E-coomerce platform like Amazon. I think that is their end game and they will become a run of the mill food delivery competitor like anyone else unless they don't achieve this goal. Getting to a unified customer platform across its acquisitions was the basic part of the grand strategy. It may seem like a risky strategy, but I think that if it pulls it off, it would become impregnable and give it a very deep wide moat. Otherwise without it, it could be easily disrupted by AI, or lose its top spot.

Management had this to say:

In addition to driving strong organic growth in 2025, we made progress across new areas that we expect will differentiate our services in the coming years, including our global technology platform, in-store services, and our autonomous delivery platform. In our U.S. restaurant category in Q4 2025, we drove double-digit Y/Y growth in the number of new consumers, as well as continued strong growth in order rates among every mature cohort. This helped drive Y/Y growth in Marketplace GOV in the U.S. restaurant category in Q4 2025 to its second-highest level in the last fifteen quarters. In 2026, we expect unit economics in the U.S. restaurant category to increase from 2025, but at a slower place than the average pace over the last three years.

The biggest surprise was in the grocery and retail categories, which is not DoorDash's strength, and a much tougher market for it do will in. I believe it will be a difficult challenge when such a large section of the market is walled off by grocery and retail chains like Walmart and Amazon.

Still management stated this:

In our U.S. grocery and retail categories in Q4 2025, we drove Y/Y growth in Marketplace GOV that was consistent with Y/ Y growth in Q3 2025 and was above our Y/Y growth in Q4 2024. We attracted more new consumers to our U.S. grocery and retail categories in Q4 2025 than in any previous quarter, drove initial engagement among our newer cohorts7 that increased Y/Y, and drove strong growth in order rates among our mature cohorts. In total, over 30% of our U.S. MAUs and nearly 30% of our global MAUs engaged with our grocery and retail categories in December. Unit economics in our U.S. grocery and retail categories increased on both a Y/Y and Q/Q basis in Q4 2025. We currently expect unit economics in our grocery and retail categories to turn positive in 2H 2026.

I reiterate that DoorDash should sell for 30x2028 adjusted earnings of 10.30. That works out to an annualized return of 24%.