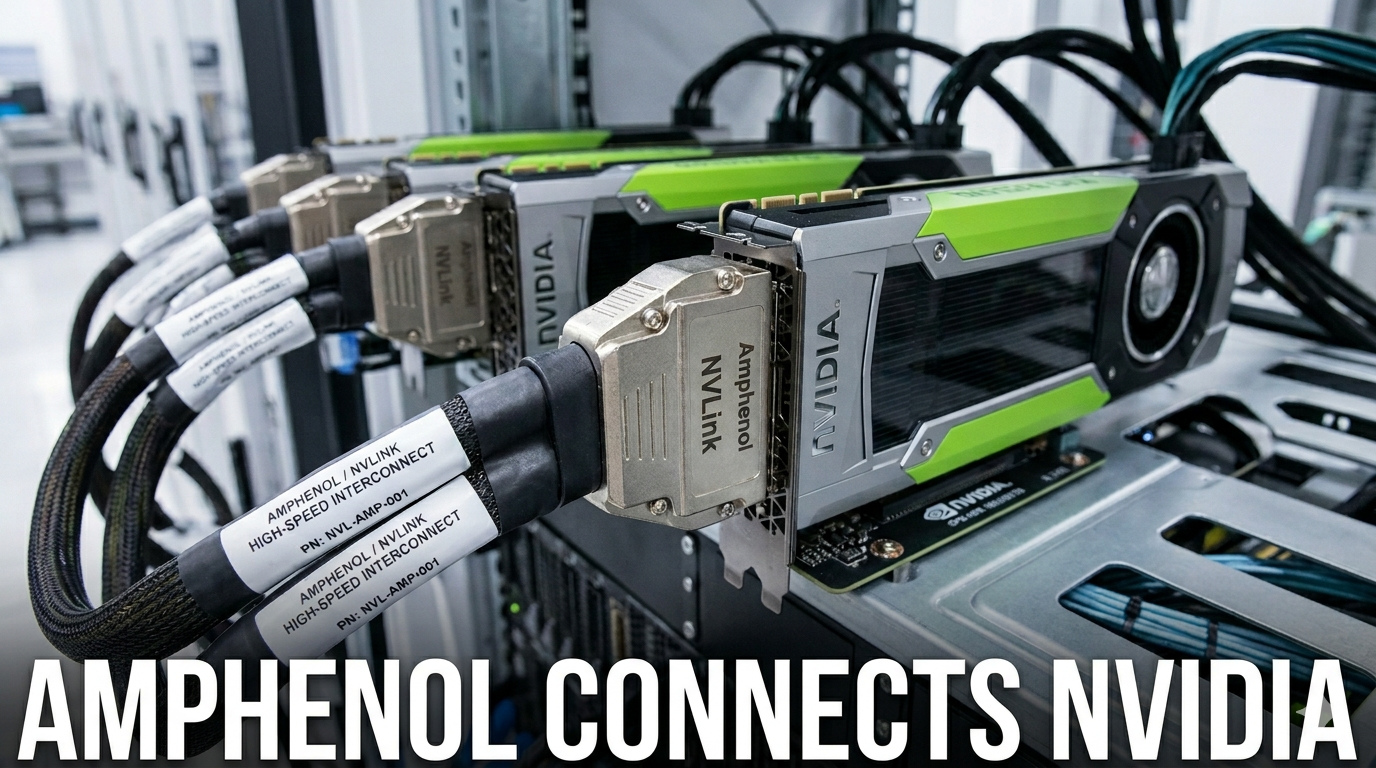

Amphenol's IT datacom segment is fueled by hyperscaler AI data center capex and its role as Nvidia's primary connector supplier. Buy on declines.

Amphenol (APH) $127

Industry/Sector/Type - Industrial, communications, defense and aerospace

Biggest catalyst for the stock - Amphenol's IT datacom segment is fueled by hyperscaler AI data center capex and its role as Nvidia's primary connector supplier.

I like the company, it is worth accumulating starting at this price and then on declines. Their overall execution and Nvidia’s partnership for the NVLink systems are good reasons to accumulate the stock.

1 Year 74% 5 Year 313% 10 Year 904% - This pretty stellar, though the vast majority of the gains have come in the past year, inflating the longer-term performance, the stock was in neutral for a long time.

All growth estimates are three years forward, measured against its forward multiple.

P/S 5 Sales Growth 20% P/S Growth 0.25

P/E 28 Earnings Growth 23% PEG 1.2

Cash Flow Margin 30%

Operating Margin 26%

I will be buying the stock on declines.