Advantest's stellar quarterly performance with a net income beat of 64% and revenue beat of 26% confirmed the AI revolution's strong growth.

Advantest - (ATEYY) $191- the world's largest semiconductor tester with over 60% market share reported insane quarterly earnings, with a 64% jaw dropping surprise! It has been a core holding for more than three years and I continue to hold it.

Advantest reported financial results on January 28, 2026, that far exceeded market consensus:

Advantest indicated that the good times are likely to continue sharply increased its full-year FY2025 forecast: (Advantest has a March year ending, its fiscal 2025 ends March 2026).

[caption id="attachment_6801" align="alignnone" width="1286"] Advantest_Financial_Forecast[/caption]

Advantest_Financial_Forecast[/caption]

Advantest is a critical "picks and shovels" play for the AI boom. As AI chips (GPUs and custom ASICs) become more complex, they require more intensive testing, which directly benefits Advantest's high-end SoC (System-on-Chip) testers. The company forecasts the SoC tester market will grow to $8.5–$9.5 billion in 2026, a massive leap from earlier projections.

[caption id="attachment_6802" align="alignnone" width="1286"] Advantest_Semi_Testing_Market_Size[/caption]

Advantest_Semi_Testing_Market_Size[/caption]

The Memory Tester segment also saw a 31% quarter-over-quarter increase, driven by the demand for high-bandwidth memory (HBM) used in AI servers.

There is no let up in sight at least for another year, and management indicated that digestion remains a myth, gladly! as the expected slowdown never materialized and instead demand remained robust. It also guided to 30-40% revenue growth in FY2026, driven by AI, GPU, and custom ASIC markets. Management has a reputation of being conservative, and I suspect that these forecasts too would likely be beat and growth will continue. Given strong inferencing needs and the emphasis on expanding the entire AI chip market by both GPUs and ASICs it stands to reason that the automated test equipment (ATE) market will continue to grow. After all at least $500Bn in Capex is expected towards AI 2026, and likely to continue to 2030, and it stands to reason that a fair chunk will also go to the tester. At some point, a 14x sales and 50x earnings multiple will start biting and investors should gear up to encash 20-25% as profit.

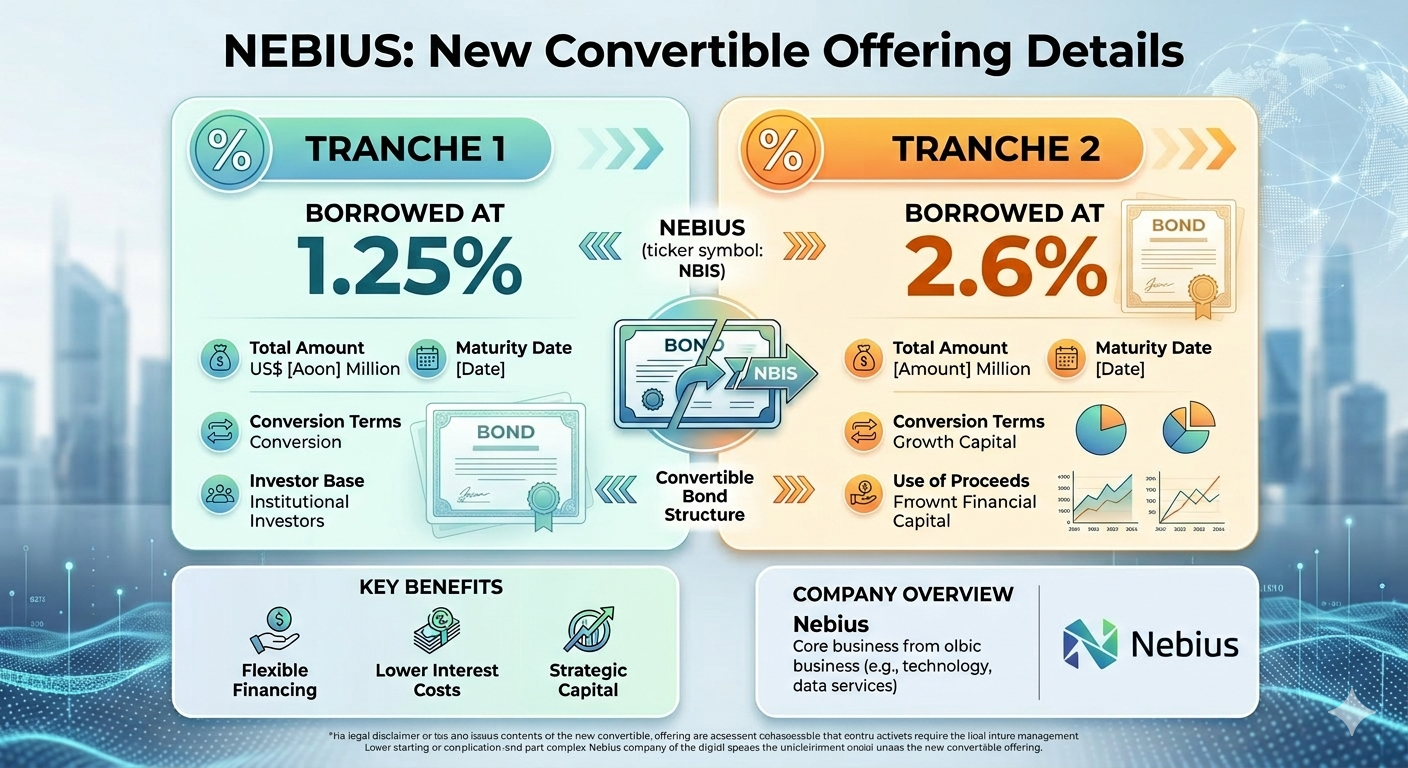

Nebius' masterly execution as an integrated neocloud player allows it to borrow at very cheap interest rates with very little shareholder dilution.