Wells Fargo's asset cap removal should lead to growth in its lending business, and earnings. The stock is still reasonably priced

Wells Fargo (WFC) $84. I bought shares around $86 yesterday, and plan to add on declines.

Industry/Sector/Type - - - Big Money Center/Banking/Cyclical

Biggest catalyst for the stock - Resumption of growth with a reasonable valuation after the removal of a Fed imposed asset cap.

One of the beneficiaries of the 2009 Great Financial Crisis bailout, WFC was strapped by higher capital requirements, restricted dividends and buybacks. However, even as controls were being lifted, WFC sunk further into the ground by poor management, leading it to be restrained from growth for a long time by regulators, following a legal fallout of overstating earnings, and bad business practices.

As a result its stock has only returned 52% in the last 10 years, unlike peers JPM, BAC who’ve done better with 365%, and 204% respectively.

Positives

Shackles removed: In June 2025 the Federal Reserve officially lifted the $1.95 trillion cap, which it had imposed in February 2018 following the bank’s fake-account and sales-practice scandals. This limit had prevented Wells Fargo from increasing its loan book and balance sheet until it cleaned up its act and inculcated better governance and risk management practices.

Better performance: As a result, Wells Fargo & Company delivered strong Q3 2025 results, with resilient credit quality to boot. WFC's NII, net interest income rose 2% YoY, non-interest income 9.3%, and credit costs declined 25%, driving net income up 9% and EPS up 17%, indicating a larger interest spread and operating leverage. This augurs well for continued earnings growth.

Management believes that it can deliver better returns on capital targeting a higher ROTCE (17-18%) and return money to shareholders via dividends and share buybacks.

Its loan book should also increase substantially after the asset cap removal.

WFC trades at 1.6x book value, compared to 1.8, and 1 for JPM and BAC respectively, and 12x earnings with a 9% growth, compared to 14x earnings for JPM with only 5% growth, though BAC is the cheapest at 12x earnings with 10% growth.

Negatives

The stock has done well this year with a 31% gain, and likely to consolidate for a while.

It also needs to be disciplined and not fall into growing at all costs and racking up credit losses, just because its asset cap has been removed.

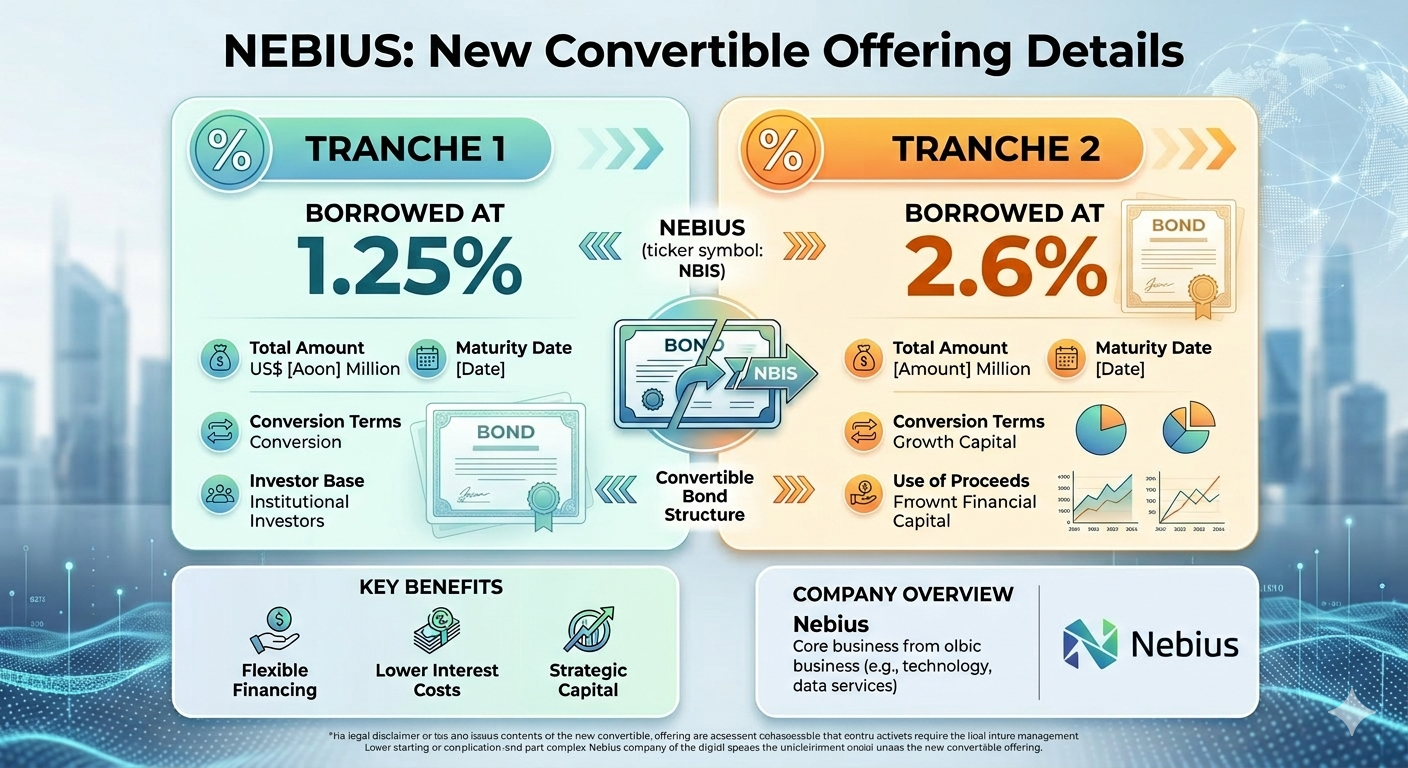

Nebius' masterly execution as an integrated neocloud player allows it to borrow at very cheap interest rates with very little shareholder dilution.